Between September 2011 and mid-2012, an unprecedented wave of resignations swept through the global financial industry. CEOs, board members, chief investment officers, and senior executives at major banks and financial institutions departed their positions at a rate that far exceeded normal turnover patterns. The number of documented departures ultimately reached 358, nearly triple the initial count of 122 that first drew public attention to the phenomenon.

The Statistical Anomaly

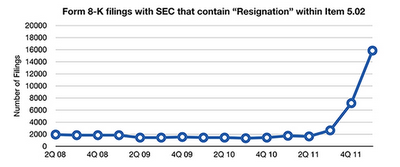

The initial question when the resignations began attracting attention was whether the numbers were actually unusual. With thousands of financial institutions operating worldwide, some turnover is expected. To establish a baseline, researchers examined resignation filings submitted to the U.S. Securities and Exchange Commission under the Securities Exchange Act of 1934, tracking the data back to 2008.

The results were striking. The rate of resignations filed with the SEC showed a dramatic spike beginning in the second and third quarters of 2011, far exceeding the established three-year baseline. This statistical departure from normal patterns suggested that something beyond routine career transitions was driving the exodus.

The Scale and Geographic Spread

The resignations spanned virtually every major financial center on earth. Departures were documented at institutions across the United States, United Kingdom, Europe, Asia Pacific, the Middle East, Africa, and Latin America. The list included some of the most powerful positions in global finance.

Among the most notable departures during this period:

- Bank of New York Mellon: CEO Robert P. Kelly resigned in September 2011

- European Central Bank: Governing board member Jurgen Stark resigned September 2011; President Jean-Claude Trichet departed October 2011; Executive Board member Lorenzo Bini Smaghi resigned November 2011

- Morgan Stanley: Chairman John Mack resigned September 2011

- UBS: CEO Oswald Gruebel quit following a rogue trader crisis in September 2011; co-chiefs of global equities Francois Gouws and Yassine Bouhara departed in October; Japan Investment Banking Chairman Matsui resigned in November

- Goldman Sachs: Asia Pacific co-head Yusuf Alireza retired November 2011; Executive Director Greg Smith resigned publicly in March 2012, writing an op-ed in the New York Times denouncing the firm’s culture

- World Bank: President Robert Zoellick announced his resignation in February 2012

- Citigroup: Japan CEO Darren Buckley resigned December 2011; multiple senior executives departed in subsequent months

- HSBC: Multiple resignations across its Israeli desk, Bermuda operations, and other divisions

- Royal Bank of Scotland: CEO Stephen Hester resigned

- Bank of India: CEO and Managing Director stepped down

- Central Bank of Jordan: Governor Faris Sharaf resigned over policy disagreements

- Central Bank of Latvia: Chief banking regulator Irena Krumane resigned after a major bank fraud was uncovered

- International Monetary Fund: Europe Director Antonio Borges resigned November 2011

The resignations were not limited to banks. Pension fund managers, hedge fund directors, insurance company executives, and regulatory officials were all part of the wave. State pension funds in South Carolina, New Mexico, and other states saw key personnel depart. Securities regulators in Sri Lanka, Latvia, and other countries also experienced turnover.

Patterns Within the Data

Several patterns emerged from the resignation data. First, the departures clustered around institutions with significant exposure to European sovereign debt. Dexia, the Franco-Belgian bank with large positions in peripheral European government bonds, saw its CEO and chairman both depart during this period. Multiple ECB officials left during the same timeframe.

Second, several resignations followed scandals or regulatory actions. UBS lost multiple senior executives after a $2.3 billion unauthorized trading loss. Citibank Japan’s CEO departed after the bank received its third regulatory punishment in seven years. A cooperative bank in India saw its CEO arrested for embezzlement. These departures, while tied to specific causes, added to the overall volume.

Third, many departures cited vague “personal reasons” without further explanation, a pattern that attracted suspicion given the sheer number using identical language.

Theories Behind the Exodus

The unprecedented scale of the departures generated several competing explanations:

Anticipation of Financial Collapse: The most widely discussed theory held that these executives possessed insider knowledge of an impending financial crisis and were positioning themselves to avoid accountability. By resigning before a collapse, they would be distanced from the institutions they had managed when the consequences materialized. The 2008 financial crisis had demonstrated how quickly public outrage could focus on banking executives, and those who remained in their positions bore the brunt of congressional investigations, regulatory actions, and public scrutiny.

Regulatory Pressure: The post-2008 regulatory environment, including the Dodd-Frank Act in the United States and similar reforms in Europe, imposed new compliance burdens and personal liability provisions on senior financial executives. Some departures may have reflected executives concluding that the increased personal risk was no longer worth the compensation.

European Sovereign Debt Crisis: The escalating crisis in Greece, Portugal, Ireland, Spain, and Italy created enormous uncertainty for financial institutions with exposure to European government bonds. Executives at exposed institutions may have calculated that departure was preferable to navigating the fallout from potential sovereign defaults.

Normal Turnover Amplified by Attention: Skeptics argued that once researchers began tracking resignations, confirmation bias led them to record departures that might otherwise have gone unnoticed, artificially inflating the apparent significance of the trend. However, the SEC filing data, which measured departures against a consistent baseline, undercut this explanation by demonstrating a genuine statistical spike.

The Information Asymmetry Problem

Regardless of which theory best explains the departures, the phenomenon highlighted a fundamental asymmetry in the financial system. Senior executives at major institutions have access to information about systemic risks, counterparty exposures, and institutional health that is not available to the public, to regulators in real time, or even to their own shareholders.

When hundreds of such individuals simultaneously choose to leave their positions, the information signal is unmistakable even if its specific content remains opaque. The executives were acting on knowledge that the general public did not possess. Whether that knowledge concerned imminent institutional failures, coming regulatory crackdowns, or structural problems in the global financial system, the scale of the departures indicated that something significant was known within the upper echelons of global finance that had not been communicated to the markets or the public.

What Followed

The years following the resignation wave saw several of the feared scenarios partially materialize. The European sovereign debt crisis intensified, requiring bailouts for multiple countries. Several banks that experienced executive departures during this period subsequently reported significant losses or underwent restructuring. The regulatory environment continued to tighten, with increased enforcement actions and personal penalties for financial executives.

However, the complete systemic collapse that some predicted did not occur, largely due to unprecedented central bank interventions including quantitative easing programs by the Federal Reserve, European Central Bank, and Bank of Japan. Whether those interventions merely postponed the reckoning that the departing executives foresaw, or whether they successfully resolved the underlying problems, remains a matter of debate among economists and financial analysts.

The 2011-2012 banking resignation wave stands as one of the largest coordinated departures of financial industry leadership in modern history. The 358 documented resignations across dozens of countries and hundreds of institutions represented an unmistakable signal that those with the deepest knowledge of the global financial system were choosing to step away from their positions at a rate and pace that defied normal explanation.