§ 2 — The Suppression

The December 9, 1968 judgment was a problem for a bank. The usual response to a legal problem is to appeal it. The bank tried. What happened next is the part of the Credit River story that most secondary accounts get wrong, and getting it wrong matters, because the errors are exactly the kind of thing that discredits the underlying doctrine when someone tries to cite it in court.

This section covers the eighteen months between Mahoney's December ruling and the case's actual end in June 1970. No court ever reversed either Mahoney judgment on the merits. The case was not overturned. It was neutralized through five distinct procedural mechanisms, none of which involved anyone rebutting Lawrence Morgan's sworn testimony or addressing Mahoney's legal analysis.

Here is what actually happened.

The Bank Tried to Appeal. The Appeal Was Never Perfected.

Between December 10 and December 20, 1968, First National Bank of Montgomery filed its notices of appeal, sureties, and affidavits. That is the paperwork a party files when it intends to take a judgment to the next level. Standard procedure.

There was a statutory requirement the bank had to satisfy first. Under M.S.A. 532.38, subdivision 4, a party appealing from a justice-of-the-peace court had to pay $2 to the court clerk within ten days of judgment. The statute was specific and unambiguous. Without the fee paid in proper form, the appeal did not lawfully exist. It had no legal effect. There was nothing for a district court to hear.

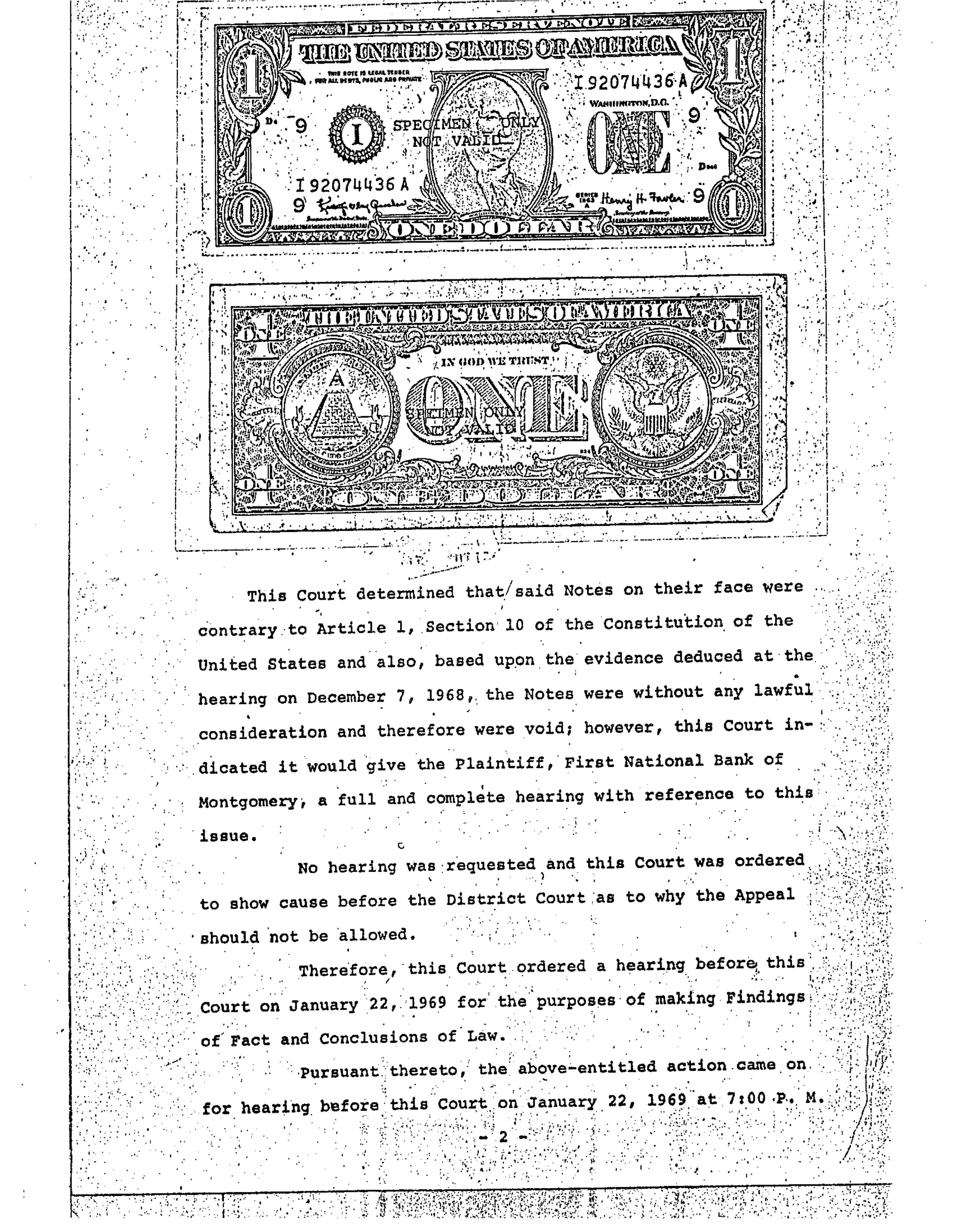

The bank submitted the $2. It tendered two Federal Reserve Notes, two $1 bills.

On January 6, 1969, Justice of the Peace Martin V. Mahoney issued a Notice of Refusal to Allow Appeal. He ruled that Federal Reserve Notes were not lawful money for purposes of satisfying the statutory fee requirement, and he explained why at length.

His constitutional ground was Article 1, Section 10 of the U.S. Constitution: "No State shall make any thing but Gold and Silver Coin a Tender in Payment of Debts." Mahoney's analysis connected that clause to the specific transaction. The Clerk of the District Court is an officer of the Judicial Branch of the State of Minnesota. When the clerk accepts a payment, that is an act of the State of Minnesota. The Constitution prohibits States from making anything but gold and silver coin a tender in payment of debts. Therefore, the State of Minnesota cannot lawfully accept Federal Reserve Notes as tender for a statutory court fee.

The two notes the bank had submitted, one bearing Serial No. L12782836 and the other a Minneapolis Federal Reserve Bank issue, were ruled "not lawful money within the contemplation of the Constitution of the United States and are null and void."

Mahoney's ruling was not a closed door. He explicitly offered the bank a path forward. His notice stated: "If Plaintiff will file a brief on the Law and the Facts with this Court within 10 days, or if Plaintiff will file an application for a full and Complete hearing before this Court on this determination a prompt hearing will be set." If the bank could satisfy him that Federal Reserve Notes were in fact lawful money issued in pursuance of and under the authority of the Constitution, he said he stood "ready and willing to reverse himself in this determination."

The bank had ten days. It used none of them.

It filed no brief. It made no application for a hearing. It did not contest the constitutional analysis or attempt to introduce any authority holding that FRNs satisfied the Article 1, Section 10 tender requirement. Instead, on January 15, 1969, the bank filed an Affidavit of Prejudice.

The bank's appeal was never lawfully perfected from that moment forward. Every procedural move that followed was built on top of an appeal that had no lawful foundation.

The Bank Filed an Affidavit of Prejudice.

Nine days after Mahoney's Notice of Refusal, First National Bank of Montgomery invoked a separate procedural tool: the Affidavit of Prejudice. Under Minnesota procedure, a party who swears that the presiding judge is prejudiced can trigger reassignment to a different judge before a hearing occurs. The affidavit does not require proof of actual bias. Filing it is enough to require transfer.

It moves fast, and in this case it produced the desired result the very next day.

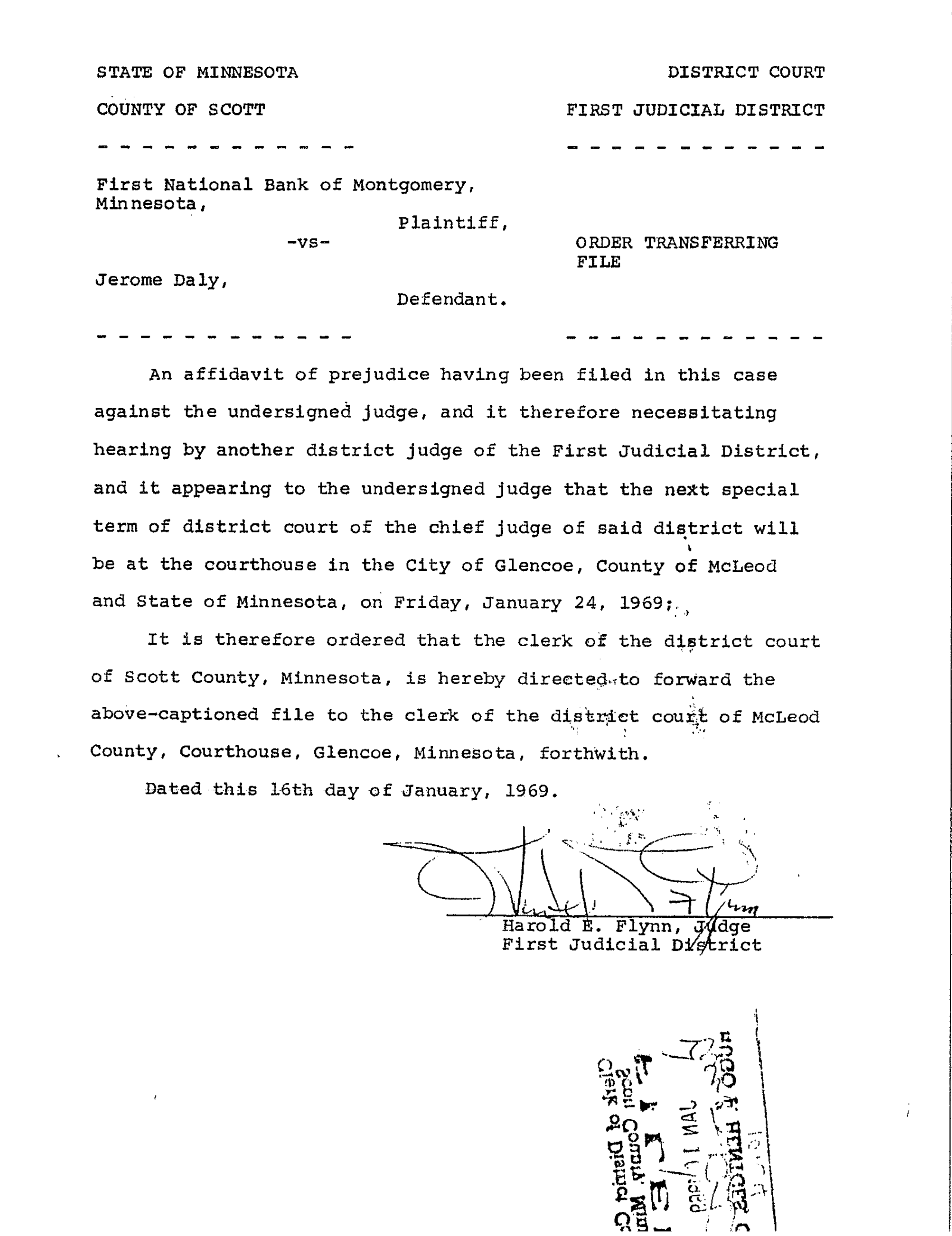

On January 16, 1969, District Judge Harold E. Flynn of the First Judicial District of Minnesota signed an Order Transferring File. The order directed Hugo L. Hentges, Clerk of District Court of Scott County, to forward the entire First National Bank of Montgomery v. Jerome Daly file to McLeod County, specifically to the courthouse in Glencoe, for hearing at the chief judge's next special term on January 24, 1969.

The order is one page. Its substance is procedural. It recites that an affidavit of prejudice was filed against the presiding judge and that hearing by another district judge of the First Judicial District is therefore necessary. Then it directs the transfer. That is all it does.

Judge Flynn did not address Mahoney's January 6 ruling on the Federal Reserve Notes. He did not address whether the bank's appeal had been lawfully perfected under M.S.A. 532.38. He did not address the constitutional question Mahoney had raised about Article 1, Section 10. He did not address the underlying merits of the December 9 judgment at all. The order treats the case as if it is a live appeal properly before the District Court, without examining whether the precondition for that posture had been satisfied.

That precondition had not been satisfied. Mahoney had said so on January 6. The question was whether Mahoney would accept the transfer, or whether he would hold that the transfer order itself was void for lack of jurisdictional foundation.

He held that it was void.

Mahoney Refused the Transfer.

On January 20, 1969, Ralph Hendrickson, cashier of First National Bank of Montgomery, was served with a Motion and Order to Show Cause setting a hearing before Mahoney's court at 7:00 PM on January 22, 1969. Mahoney was not treating the case as transferred. He was proceeding as if his court retained jurisdiction.

The bank was served four days before the hearing. It did not appear. It did not contact the court to request a continuance. It did not send a representative or an attorney. Mahoney waited one full hour in his courtroom on the evening of January 22. Then he proceeded, taking testimony from Daly, who appeared without the bank being present.

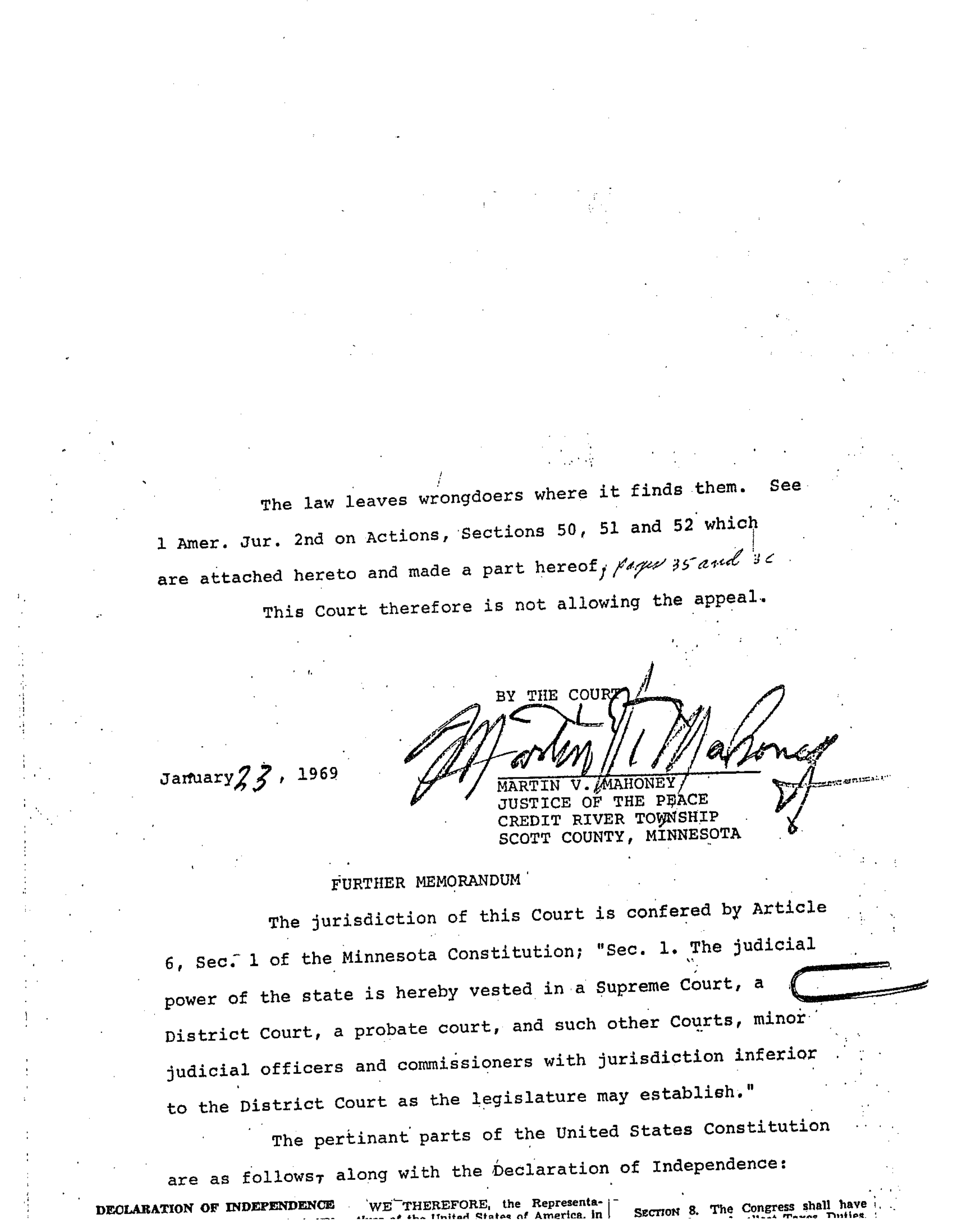

The next day, January 23, 1969, Mahoney issued Supplemental Findings of Fact, Conclusions of Law, and Judgment from the Justice Court of Credit River Township, Scott County. It is the second Mahoney ruling in this case, and in some respects the more doctrinally significant one.

The supplemental judgment opens by narrating the full sequence of events from December 7, 1968 forward: the trial, the original judgment, the Notice of Refusal, the service of Hendrickson, the bank's non-appearance at the January 22 hearing. It then proceeds to its numbered conclusions.

First conclusion: the original December 9, 1968 judgment is confirmed in all respects.

Second conclusion: the two Federal Reserve Note bills tendered as the appeal fee are declared "null and void for any lawful purpose." They are not lawful money, they are in violation of the Constitution, they are "not valid for any purpose." The Notice of Refusal to Allow Appeal is made absolute.

Third conclusion: jurisdiction. This is the core holding that Mahoney used to reject Judge Flynn's transfer order.

"I hold that this case has not been lawfully removed from this Court and Jurisdiction thereof is still vested in this Court."

The reasoning: M.S.A. 532.38 required $2 in lawful tender to perfect the appeal. The bank tendered Federal Reserve Notes that Mahoney had already ruled were not lawful tender. An appeal that was never lawfully perfected confers no jurisdiction on the District Court. Without that jurisdictional foundation, Judge Flynn's transfer order had no legal effect. The case had not left Mahoney's court. It was still in his court.

Fourth conclusion: the bank was estopped from challenging Mahoney's jurisdiction at all. First National Bank of Montgomery had filed the original action in Mahoney's justice court. It had invoked that court's jurisdiction voluntarily. Having asked Mahoney's court to decide the dispute, the bank could not now turn around and claim the court had no authority over the proceeding.

Mahoney then extended his constitutional analysis well beyond what the December 9 judgment had said. The supplemental judgment is where his findings reach their broadest scope:

"The Federal Reserve and National Banks exercise an exclusive monopoly and privilege of creating credit and issuing their Notes at the expense of the public, which does not receive a fair equivalent. This scheme is for the benefit of an idle monopoly and is used to rob, blackmail and oppress the producers of wealth."

And on the banking statutes directly:

"The Federal Reserve Act and the National Bank Act is in its operation and effect contrary to the whole letter and spirit of the Constitution of the United States; confers an unlawful and unnecessary power on private parties; holds all of our fellow citizens in dependance; is subversive to the rights and liberties of the people. It has defied the lawfully constituted Government of the United States. The two banking acts and Sec. 462 of Title 31, U.S.C., are therefore unconstitutional and void."

He also ruled that Title 31 U.S.C. Section 462, which attempts to make Federal Reserve Notes legal tender, is in direct conflict with the Constitution and is therefore unconstitutional and void. He cited Title 12 U.S.C. sections 411, 412, 417, 418, and 420, among other authorities, in support of his analysis.

The December 9 judgment had found that this specific note and mortgage lacked lawful consideration. The January 23 judgment declared the Federal Reserve Act and the National Bank Act unconstitutional and void in their entirety.

Neither ruling was ever reviewed on the merits by any appellate court.

The situation after January 23 was this: Mahoney's court held that the case had not left his court, and he had just issued his most sweeping findings yet. Judge Flynn's court held that the file had been transferred to McLeod County. The Minnesota Supreme Court had not weighed in. No one had resolved the jurisdictional conflict. The bank's appeal remained unperfected.

The Minnesota Supreme Court Dismissed — But Never Ruled.

On April 15, 1969, the Minnesota Supreme Court took the only direct action it ever took on the First National Bank of Montgomery v. Daly file.

Associate Justice Walter F. Rogosheske signed the order. It is one sentence: "Pursuant to said motion, and upon all of the files herein, IT IS ORDERED that the appeal be, and hereby is dismissed."

The caption of the order reads: "First National Bank of Montgomery, Respondent vs. Jerome Daly, Appellant" — case no. 41929. Daly was the appellant. The bank had moved to dismiss Daly's appeal, and the court granted the motion. Mae Sherman, Clerk of the Supreme Court, filed the order the same day.

The bank's own appeal, the one Mahoney had rejected on January 6 for tendering Federal Reserve Notes as the statutory fee, never reached the Minnesota Supreme Court. It was never lawfully perfected. What the Supreme Court dismissed was Daly's separate appeal, apparently from some adverse District Court ruling that occurred after Judge Flynn's January 16 transfer order. Daly was apparently appealing something that went against him in the district-court proceedings that followed the file transfer.

The standard framing of Credit River's legal history says the Minnesota Supreme Court reversed Mahoney's ruling. That is not what this order is. The order contains no merits analysis. It has no discussion of lawful consideration, no discussion of Federal Reserve Notes as legal tender, no analysis of JP-court jurisdiction, and no assessment of either the December 9 or January 23 Mahoney judgments. It is a one-sentence procedural dismissal of Daly's appeal, issued on the bank's motion, with no reasoning whatsoever.

The two Mahoney judgments received no appellate review from the Minnesota Supreme Court, or from any other court.

They Came at Mahoney Through a Different Case.

The April 15 dismissal closed the only Supreme Court path the file had ever found. The bank's own appeal had been unperfected since January. Daly's appeal had just been dismissed without reasoning. The jurisdictional conflict between Mahoney's court and Judge Flynn's transfer order was unresolved and apparently going nowhere. By spring 1969, the bank had exhausted its direct procedural options against the Credit River file.

The next move came from outside the Credit River docket entirely.

Jerome Daly, following the December 1968 win, had brought a similar case in Mahoney's court: Leo Zurn v. Roger D. Derrick and Northwestern National Bank of Minneapolis. Same legal theory, same JP court, same judge presiding. The defendant bank in that case was not First National Bank of Montgomery. It was Northwestern National Bank of Minneapolis, a substantially larger institution.

Northwestern took a different approach than the Montgomery bank had. Rather than attempting to work through the statutory appeal process that had failed in Credit River, Northwestern petitioned the Minnesota Supreme Court for a writ of prohibition, which is an order from a superior court directing an inferior court to stop acting outside the bounds of its jurisdiction. This is a common-law mechanism for supervising courts that are operating beyond their statutory authority.

On July 11, 1969, Justice C. Donald Peterson, acting on behalf of the Minnesota Supreme Court, issued an order staying all proceedings in Mahoney's JP court in the Zurn case pending determination of Northwestern's writ petition. The stay was clear and direct: Mahoney's court was not to proceed with the Zurn case until the Supreme Court resolved whether a writ of prohibition should issue.

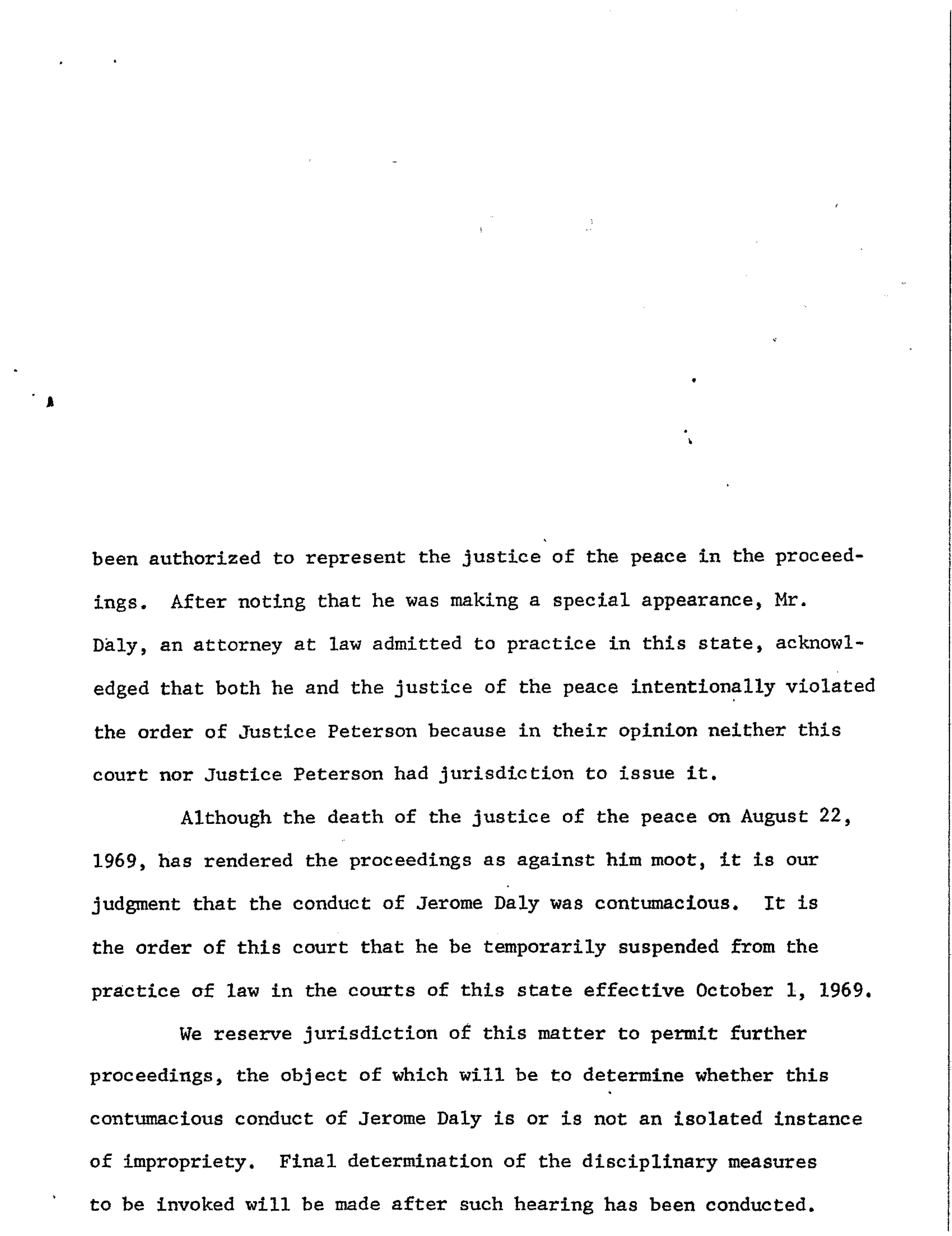

On July 14, 1969, Mahoney held a hearing in the Zurn case and entered findings of fact, conclusions of law, and an order for judgment in favor of Zurn. He did this three days after being served with Peterson's stay order.

On August 21, 1969, Jerome Daly appeared before the Minnesota Supreme Court and acknowledged that both he and Mahoney had intentionally violated the stay. His defense was that in their judgment, neither the Supreme Court nor Justice Peterson had jurisdiction to issue the stay in the first place. They believed that justice-of-the-peace courts occupied a constitutional status that placed them outside Supreme Court supervisory authority. The Supreme Court, in its later contempt opinion, characterized this reasoning as "fanciful notions that justice of the peace courts have a constitutional status giving them immunity from the jurisdiction of the supreme court."

Daly's legal analysis about JP-court independence from Supreme Court supervisory authority was the same reasoning that had animated the January 23 supplemental judgment. In Mahoney's view, the Supreme Court could not stay proceedings in a JP court because the Supreme Court lacked jurisdiction over JP courts in matters where the JP court's own jurisdictional question was at issue.

The contempt vehicle the court used to respond was not Bank of Montgomery v. Daly. It was a separate proceeding: In re Jerome Daly, Sp. 42174. The Credit River case was not the subject of the contempt. Zurn v. Derrick was. This distinction matters for understanding what the contempt opinion was and was not about.

Mahoney Died on August 22, 1969.

The per curiam opinion in In re Jerome Daly, issued September 5, 1969, contains a line about Mahoney: "the death of the justice of the peace on August 22, 1969 has rendered the proceedings as against him moot."

August 22, 1969. The proceedings against Mahoney personally were dropped because he had died.

You may have read that Mahoney was poisoned, or that his death was suspicious. The Minnesota Supreme Court opinion gives no cause of death, and no document in the primary docket of First National Bank of Montgomery v. Daly mentions a cause of death. Without a death certificate, coroner's report, or contemporaneous newspaper coverage, the cause is unverified, even if the timing invites suspicion. The contempt proceedings had been ordered on August 12, 1969. Daly's appearance before the court was August 21. Mahoney died the following day. The court mooted the proceedings against him. That is what the primary record shows.

What may have happened is a separate question from what the documents establish. Anyone citing Mahoney's death as assassination should understand that the primary record contains nothing to support that characterization.

Daly Was Suspended — for Contempt in the Other Case.

The September 5, 1969 per curiam opinion in In re Jerome Daly (Sp. 42174) addressed the contempt that remained live after Mahoney's death. Daly had acknowledged the intentional violation on August 21. His justification, that the court lacked jurisdiction to issue the stay, did not amount to a defense.

Before reaching the question of discipline, the court analyzed the Zurn complaint in detail and identified six separate jurisdictional defects placing it outside JP-court statutory authority under Minn. St. sections 530.05, 531.03, 531.04, and 532.29. The summons was returnable at 7:00 PM rather than between 9:00 AM and 5:00 PM. The summons did not state the amount claimed. Service had been performed on Northwestern National Bank in Minneapolis, a city of more than 200,000 people. Service had been performed outside Scott County without the required 20-day continuance. The amount in controversy exceeded the $100 JP-court jurisdictional limit. And the relief sought, which was declaratory judgment, was outside JP-court equitable jurisdiction.

The court cited Smith v. Tuman, 262 Minn. 149, 114 N.W.2d 73, for the proposition that acts of a JP court in excess of its jurisdiction are nullities subject to writ of prohibition.

Then it reached Daly's conduct directly:

"We are satisfied from the record that the justice of the peace acted upon the advice and at the instance of attorney Jerome Daly. Mr. Mahoney was not admitted to practice as a lawyer. An attorney who intentionally and deliberately advises and encourages a justice of the peace or any other person to disregard an order of the Minnesota Supreme Court is guilty of contempt."

The discipline imposed was a temporary suspension.

"It is the order of this court that he be temporarily suspended from the practice of law in the courts of this state effective October 1, 1969."

The court reserved jurisdiction for further proceedings before referee Hon. E.R. Selnes, District Judge, together with the State Board of Law Examiners, to determine what final discipline should be imposed.

Three things are essential to get right about this.

First: the contempt was for the Zurn stay violation, not for anything that happened in Bank of Montgomery v. Daly. The Credit River judgment itself was never the direct subject of these proceedings. Daly's suspension did not arise from anything Mahoney or Daly did in the Credit River case. It arose from their joint decision to defy Peterson's stay order in the separate Zurn litigation.

Second: "temporarily suspended" is the opinion's exact language. Final discipline was reserved for later proceedings before the referee and the Board of Law Examiners. The outcome of those proceedings is not resolved by any primary document currently in the vault. Whether the suspension was made permanent, modified, or eventually vacated is an open question from the primary sources available. Saying Daly "was disbarred" goes beyond what the September 5 opinion actually ordered.

Third: regardless of how the final discipline resolved, the practical effect as of October 1, 1969 was complete. Daly could not practice law. He could not appear as counsel for new clients. He could not litigate Credit River-style bank-consideration cases on behalf of anyone. The doctrine had two people capable of pressing it: Mahoney, who was dead, and Daly, who was suspended. Both were gone.

The Case Ended by Stipulation.

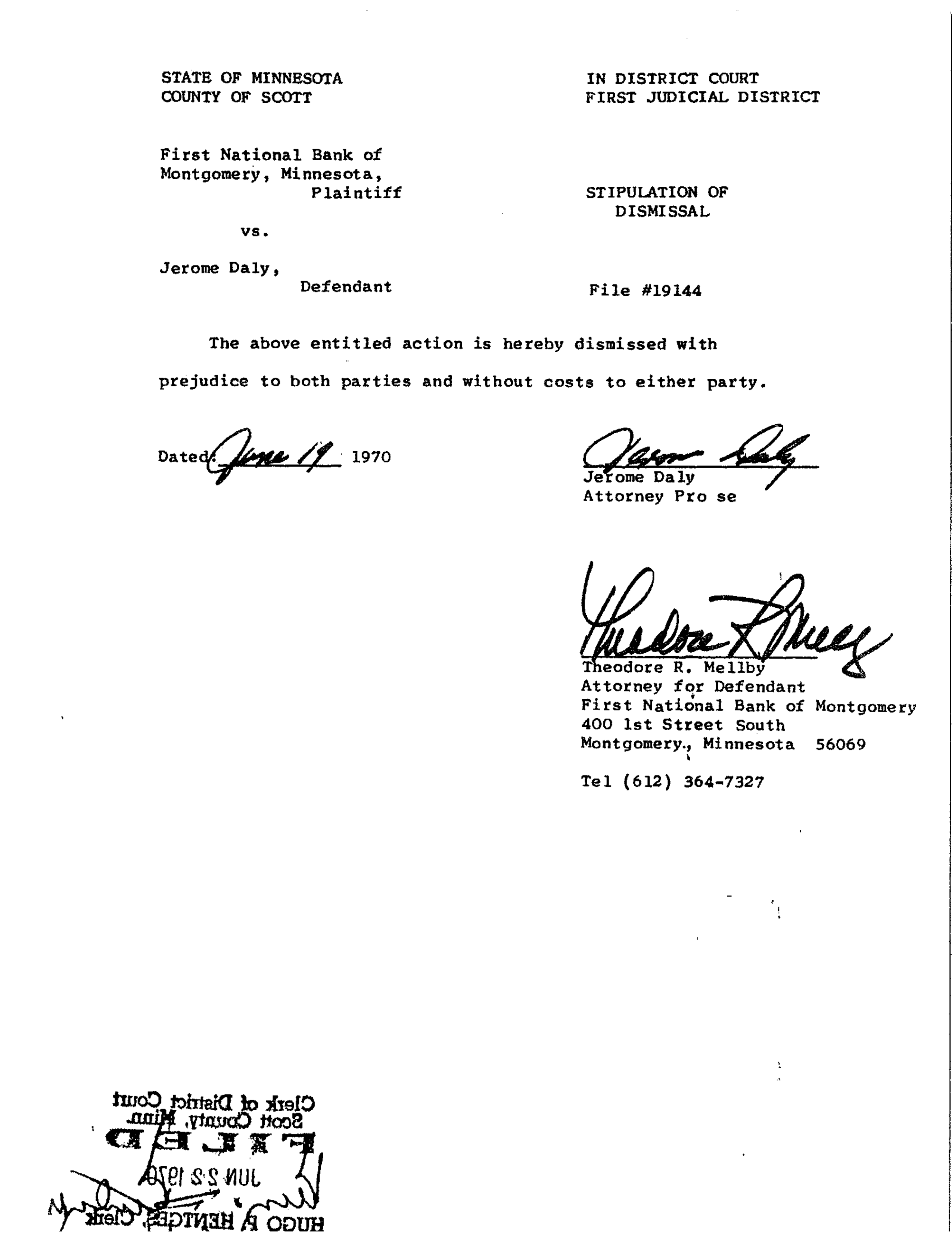

On June 19, 1970, both parties to First National Bank of Montgomery v. Jerome Daly signed a Stipulation of Dismissal.

The operative text is one sentence: "The above entitled action is hereby dismissed with prejudice to both parties and without costs to either party."

Two signatures appear on the document. Jerome Daly signed, identifying himself as "Attorney Pro se." Because his suspension had taken effect October 1, 1969, he was signing not as counsel but as a party appearing in his own right. Theodore R. Mellby signed for First National Bank of Montgomery, listing an address at 400 1st Street South, Montgomery, Minnesota. The stipulation was filed by Hugo A. Hentges, Clerk of District Court, Scott County, on June 22, 1970, as File No. 19144.

By June 1970 the arithmetic was plain. Mahoney had been dead for ten months. Daly had been suspended from practice for eight months. The bank's original appeal had been statutorily defective since January 1969 and was never cured. The jurisdictional conflict between Mahoney's court and the District Court had never been resolved by any appellate tribunal. No realistic enforcement path existed for either side. Both parties signed and walked away.

Dismissal with prejudice means neither party can refile the same claims. The bank's $14,000 claim against Daly is permanently extinguished. Daly cannot re-litigate the same counterclaim against the bank. But "with prejudice to both parties and without costs to either" is a cease-fire, not a ruling on the merits. The stipulation does not vacate Mahoney's December 9, 1968 judgment. It does not vacate his January 23, 1969 supplemental judgment. Neither of those rulings was the subject of the stipulation. They were simply left on the books, where they remain.

No appellate court reviewed the consideration question. No appellate court addressed whether Federal Reserve Notes satisfied the Article 1, Section 10 tender requirement. No appellate court reviewed Mahoney's holding that the Federal Reserve Act and the National Bank Act are unconstitutional and void. The bank obtained no appellate ruling in its favor. Daly's appeal was dismissed without reasoning. The Mahoney judgments stand exactly as he wrote them.

The suppression was real. What it did not include was any substantive rebuttal. Lawrence Morgan testified under oath that his bank created $14,000 from a bookkeeping entry and could cite no statute authorizing the practice. That testimony was never disputed on the merits in any court. Mahoney's legal analysis of those facts was never addressed by any court with authority to reverse it.

The mechanism that neutralized Credit River was not a better argument. It was the removal of the two people capable of pressing the doctrine forward, through Mahoney's death and Daly's contempt suspension in a separate case. Once both were gone, the parties signed a piece of paper and the case ended.

That is the record. § 3 addresses what survives it.