I’m finishing up a novel, a piece of speculative fiction in a genre you could call “economic-thriller”.

The Mark of the Beast?

In the book, the dollar crashes in a hyperinflationary fire (natch), replaced by a new currency called the american. The exchange rate at the time of the changeover is $1,000 equals ₳1. To illustrate its purchasing power, ₳1 buys you a candy bar.

However, americans don’t exist as physical currency. There are no “american bills” like there are dollar bills, and no coins either. Instead, americans are a fully digital currency: They exist in the ether. You need a card—be it a credit card, debit card, or EBT card—to spend americans. And to receive americans, either from employers, customers, government, etc., you need a “central account” which is tethered to your Social Security number.

The rationale for these measures is convenience—but the implication is, no one can earn, save or spend money without the government being aware of exactly what you are doing.

Since the government can easily access all your spending and earning of americans, no one can launder money, or evade taxes, or even so much as fail to pay all their bills on time. Law-makers and politicians and pundits say it’s no big deal that the government will know everything about the citizen’s finances, because, “If you’re not doing anything wrong, you’ve got nothing to hide! If you’re paying all your bills and your taxes and your loans, you got nothing to worry about!”

Another feature of this virtual currency: With americans, you can never again be late with your bills. Payments you have to make are automatically deducted from your central account. And if you take out a loan for whatever purpose, not only is that information in your central account, but your ability to spend money is automatically prioritized: Taxes get paid first, followed by private loans, then bills, then food, then “etc.”

In the novel, law-makers use this compulsory “compliance” as a selling point for the american. “Think of the convenience! No more worrying about paying your bills—your bills are all paid for you!”

However, if you don’t have enough money for “etc.”—entertainment, booze, an ice-cream sundae with the kids, what have you—you don’t get any. And if after paying off your loans and bills there isn’t enough left over for food—then no food for you. Ditto with bills: No money for electricity, or water, or heat? Then no electricity, or water, or heat for you. And if perchance you can’t fully pay off your loans, then you are declared in “non-compliance”. And if you can’t pay off your taxes, then you are charged as being in “criminal non-compliance”—and then woe is you.

In the language of the novel, it is a “fully-compliant currency”—and it forces the people to be “fully-compliant citizens” of the dictates of the government and the banksters.

This is of course a fiction I invented for my upcoming novel—but I couldn’t help notice how lawmakers and banks are all of a sudden getting on the bitcoin bandwagon.

For something that was supposed to be a threat to the established order, which is what bitcoin and the other cryptocurrencies promised to be, the established order sure seems to be happy with it: The U.S. Senate hearings on bitcoins were pretty much ofa success for bitcoins, and banks are starting to thrownothing but lovein bitcoin’s direction. The mainstream media isn’t putting down bitcoins, as it did a few years back.

In short, and unlike what a lot of cryptocurrency proselytizers have been saying—that the powers that be would beagainstbitcoins—the establishment seems to be fullyin favor—or at least accepting—of bitcoins.

Makes you goHmm . . ., now doesn’t it?

Me, I’ve already explainedhereandherewhy I think that bitcoins are in a bubble, and why bitcoins and other cryptocurrencies will never be currencies per se, only an asset class. My thinking is, cryptocurrencies represent a new class of assets whose value is highly unstable so long as they are not actually tethered to some good or service people both need to buy and have to sell. Until that day happens, cryptocurrencies are nothing but speculative investments that can plummet to zero at a moment’s notice.

However, thinking about cryptocurrencies from the point of view of the Federal Reserve, or a senator on the Banking Committee, or a trader at a bank’s prop desk, cryptocurrencies such as bitcoin have a lot of advantages—they’re not something to be dismissed out of hand.

All of bitcoin’s benefits to the establishment revolve around its blockchain.

In simple terms, a blockchain is a registry of all transactions carried out in bitcoins. Thus is resolved the problem of double-spending one particular bitcoin: It can’t be done (at least in theory) due to the blockchain.

But the blockchain is in fact a register—a trail—of bitcoins. So it’s a relative cinch to piece together each and every transaction of any particular wallet in the bitcoin universe. And since exchanges need detailed personal information about a bitcoin user in order to comply with money-laundering laws before issuing a new user with a wallet, the government or other interested parties could determine what any one particular person has been doing in the bitcoin marketplace.

In other words: Imagine that the government knew each and every cent you earned and spent, without a single exception.

That cannot be done with dollars, at least not easily. The dollar’s inefficiencies when compared to bitcoin or any other cryptocurrency are exactly what make tracking dollar transactions so hard. That’s why money-laundering in fact exists: Criminals are taking advantage of inefficiencies in the dollar to hide their profits and thus not get caught.

But with bitcoins as they currently exist, it is asnapto keep people compliant. Once some simple baseline limitations are imposed on users of bitcoins—such as the rules implemented by exchanges so as to comply with money-laundering laws—a user’s transactions are as transparent as glass.

Which is what a government would want, in order to get every bit of tax revenue it wants. Which is what a bank would want, in order to properly gauge the risk of a loan it is extending, and thereby maximize its profits.

Not only that, being able to track people’s spending completely, in real time, as can be done with bitcoin and conceivably every cryptocurrency, the government could easily rescind someone’s ability to earn money.

Witness how the government shut off WikiLeaks’ source of funding—took them less than a week. WikiLeaks depended exclusively on donations made via credit card payments—so by “encouraging” the credit card companies, Visa and Mastercard, to refuse to process donations to the organization, the U.S. government shut down Wikileaks justdaysafter the first big document leaks of 2010.

With bitcoin or some similar cryptocurrency, the government wouldn’t even need to take the step of contacting credi card companies to “encourage them to do the right thing”: The government could simply make any payment to a targeted group invalid. (And perhaps get a notice of whoever it was who donated to the targeted group?)

All this is to say, bitcoins and other cryptocurrencies are potentially a great step forward for a government looking to impose a Panopticon society on the American people. We can’t travel without TSA’s approval, so why not extend that power to people’s ability to interact in the economy as well? Due to the fact that, with bitcoins, there is a trail from people to their bitcoin wallet to their bitcoin usage, a trail that is relatively easy to read, the government could have this power over each and every citizen—the power to monitor and control our interactions with the economy.

Which is why bitcoin—far from being a threat—might just prove to be the fully-compliant currency the U.S. government can come to love. A currency that will let it have unfettered access to each and every financial transaction you carry out.

Is that something that we as a people want? More power to the government? Because that’s the promise of bitcoin.

Interest in digital coin system spikes dramatically after banking crisis in Cyprus, nearly tripling in value since last month

The value of individual Bitcoins has hit a record high of almost $147 as interest in the cryptographic currency, which has no central issuing bank, has exploded.

Though the value fell back later on Wednesday to $117, the value of all Bitcoins in circulation is approaching $1.4bn.

Both the volume being traded and the amounts being paid have suddenly risen, apparently as interest in the system has been spiked by the banking crisis in Cyprus – which had the spillover effect of making people in some southern European countries worry that their banking deposits might not be safe.

Some are thought to have converted that money into Bitcoins, driving a rapid rise in the apparent value of the “coins” – actually cryptographic solutions to complex equations.

As a result, the value of a Bitcoin has risen from just $13.50 in January, and around $30 a month ago, to more than $140 – though the price is fluctuating rapidly. The total value of the Bitcoins in circulation only broken through the $250m mark in January. Last November, each Bitcoin was worth $10.83.

Bitcoin’s market price since last month Photograph: blockchain.infoThe maximum possible number of Bitcoins that can exist is 21m, meaning that at present prices the currency would be worth just over $3bn. Trades can be made with fractions of Bitcoins, providing flexibility that enables transactions.

The price of each Bitcoin began rising abruptly on Tuesday 19 March, going from $47 then to $72 by 23 March. That matches the period of the Cyprus bailout almost exactly: its banks shut on Friday 15 March – and then the Cypriot government announced over the next two days that they required a bailout and that all savers’ deposits would be tapped. Though that was later revoked, with only larger deposits being subject to a 10% requisition, savers in other countries with troubled finances had already acted.

Bitcoin’s usefulness is its lack of the need for a central bank – and that the peer-to-peer network backing it allows transactions to continue as long as there are people willing to exchange the coins for something of value (or to donate them). For Europeans worried about the possibility that their banks might shut, trapping their savings inside, and not open until some amount had been skimmed from them, that makes Bitcoins suddenly attractive.

A growing number of sites online accept Bitcoins as payments for items – including some electronics sites and other less legal sites, including Silk Road, which offer drugs.

The interest, and the exponential rise in value, means that it is now worthwhile for people to devote computing power to try to “mine” Bitcoins by finding the solutions to the cryptographic challenges that underlie each coin. As Bitcoins become more valuable, the return on computing power should grow – except that Bitcoins are designed so that as more come into circulation, it becomes harder to “mine” new ones. A distributed algorithm ensures that about 1 Bitcoin is created every 10 minutes – but not more.

That is reflected in the chart from blockchain.info, showing that the growth in total number of Bitcoins in circulation has actually slowed since December 2012.

Some suggest that the rapid rise in Bitcoins’ value may mean that it will become less useful as a currency, because it becomes more attractive to hoard it than to spend it – because exchanging it for any other item or service risks losing out on the rising value. That is “hyperdeflation”, argues Joe Wiesenthal of Business Insider. It is the opposite of “hyperinflation”, like that which hit the Weimar Republic in Germany after the first world war, or Zimbabwe more recently, where the currency becomes less and less valuable for transactions. By contrast, Bitcoin is experiencing a period when it is becoming less attractive to spend it – which will make it less useful as a currency for trading.

Bitcoin Gavin Andresen announced today on the Bitcoin Talk forums that he has launched a non-profit, modeled on the Linux Foundation, that will seek to “help people exchange resources and ideas [about Bitcoin] more freely.”

If you’re unfamiliar with the Linux Foundation, it’s a non-profit aimed at promoting the growth and advancement of Linux, an open-source operating system. David Perry, author of Coding in My Sleep, describes the foundation as:

A non-profit entity explicitly designed to help Linux succeed. It does this by acting as a neutral spokesperson, building networks of Linux users and developers, promoting the use of standards to make developers’ lives easier and so on. They also sponsor a number of key developers financially, turning what would otherwise be a hobby into an actual pays-the-bills job, thus allowing the developers to remain independent and work full time on improving Linux.

Mr. Andresen has similar hopes for the Bitcoin Foundation, which will help to standardize and fund Bitcoin infrastructure, keep the currency secure, and work to correct false interpretations and misinformation about Bitcoin. Bitcoin developers and aficionados can pay for membership status, which ranges from a 2.5BTC annual membership (about $30, according to Preev) all the way up to 10,000BTC/year (about $123,000–which, whoa).

“I think Linux is a great ‘role model’ for Bitcoin,” he wrote in the announcement. “It is a very successful open source project that really embraced the notion of ‘open,’ encouraging the use of the core technology for a wide range of applications. I hope that the Bitcoin Foundation will help do the same for Bitcoin.”

Of course, the Linux Foundation is about promoting an operating system that only accounts for 1.55% of the OS market share, whereas the Bitcoin Foundation will work to promote a cryptocurrency sometimes used for blackmarket activity. Bitcoin has seen its own share of PR nightmares in recent months, from an exchange-paralyzing heist to talk of Bitcoin ponzi schemes. Perhaps the Bitcoin Foundation is just what the currency needs to clean up its image.

The Foundation itself even plainly states the need for an organization that can help break Bitcoin out of its cyberdungeon:

As the Bitcoin economy has evolved, we have all noticed barriers to its widespread adoption—botnets that attempt to undermine the network, hackers that threaten wallets, and an undeserved reputation stirred by ignorance and inaccurate reporting.

To us, it became clear that something had to be done. We see this foundation as critical for bringing legitimacy to the Bitcoin currency. Only then can we increase its adoption and positive impact on the world’s finance.

The Bitcoin Foundation has stacked its board with well-known, high-profile people active in the Bitcoin community so that users feel safe donating. Still, as Mr. Perry points out, “according to the dissenting voices, it’s representative only of the ‘big business’ side of Bitcoin, not the actual users.” Indeed, some users have expressed dissent on the boards, but for the most part they seem supportive of a unified effort to legitimize Bitcoin.

Plus, Mr. Andresen stresses that these decisions aren’t set in stone.

“The structure of the Foundation can be changed by a vote of its members,” he wrote, “and exactly what the Foundation does will largely depend on who is willing to step up do the work to make things happen.”

The FBI sees the anonymous Bitcoin payment network as an alarming haven for money laundering and other criminal activity — including as a tool for hackers to rip off fellow Bitcoin users.

That’s according to a new FBI internal report that leaked to the internet this week, which expresses concern about the difficulty of tracking the identify of anonymous Bitcoin users, while also unintentionally providing tips for Bitcoin users to remain more anonymous.

In the document, the FBI notes that because Bitcoin combines cryptography and a peer-to-peer architecture to avoid a central authority, contrary to how digital currencies such as eGold and WebMoney operated, law enforcement agencies have more difficulty identifying suspicious users and obtaining transaction records.

Though the Bureau expresses confidence that authorities can still snag some suspects who use third-party Bitcoin services that require customers to submit valid identification or banking information in order to convert their bitcoins into real-world currencies, it notes that using offshore services that don’t require valid IDs can thwart tracking by law enforcement.

Bitcoin is an online currency that allows buyers and sellers to exchange money anonymously. To “cash out,” the recipient has to convert the digital cash into U.S. dollars, British pounds or another established currency. Bitcoin is used as a legitimate form of payment by numerous online retailers selling traditional consumer goods, such as clothing and music. But it’s also used by underground sites, such as Silk Road, for the sale of illegal narcotics.

To generate bitcoins, users have to download and install a free Bitcoin software client to their computers. The software generates Bitcoin addresses or accounts — a unique 36-character string of numbers and letters — to receive Bitcoin payments. The currency is stored on the user’s computer in a virtual “wallet.” Users can create as many addresses or accounts that they want.

To send bitcoins, the sender enters the recipient’s address as well as the number of bitcoins she wants to transfer to the address. The sender’s computer digitally signs the transaction and sends the information to the peer-to-peer Bitcoin network, which validates the transaction in a matter of minutes and releases the coins for the receiver to spend or convert.

The conversion value fluctuates with supply and demand and the trust in the currency. As of last month, there were more than 8.8 million bitcoins in circulation, according to Bitcoin, with a value of about $4 and $5 per bitcoin. The FBI estimates in its report that the Bitcoin economy was worth between $35 million and $44 million.

It’s easy to see the attraction for criminals.

“If Bitcoin stabilizes and grows in popularity, it will become an increasingly useful tool for various illegal activities beyond the cyber realm,” the FBI writes in the report. “For instance, child pornography and Internet gambling are illegal activities already taking place on the Internet which require simple payment transfers. Bitcoin might logically attract money launderers, human traffickers, terrorists, and other criminals who avoid traditional financial systems by using the Internet to conduct global monetary transfers.”

Bitcoin transactions are published online, but the only information that identifies a Bitcoin user is a Bitcoin address, making the transaction anonymous. Or at least somewhat anonymous. As the FBI points out in its report, the anonymity depends on the actions of the user.

Since the IP address of the user is published online with bitcoin transactions, a user who doesn’t use a proxy to anonymize his or her IP address is at risk of being identified by authorities who are able to trace the address to a physical location or specific user.

And a report published by researchers in Ireland last year showed how, by analyzing publicly available Bitcoin information, such as transaction records and user postings of public-private keys, and combining that with less public information that might be available to law enforcement agencies, such as bank account information or shipping addresses, the real identity of users might be ascertained.

But the FBI helpfully lists several ways that Bitcoin users can protect their anonymity.

Create and use a new Bitcoin address for each incoming payment.

Route all Bitcoin traffic through an anonymizer.

Combine the balance of old Bitcoin addresses into a new address to make new payments.

Use a specialized money-laundering service.

Use a third-party eWallet service to consolidate addresses. Some third-party services offer the option of creating an eWallet that allows users to consolidate many bitcoin address and store and easily access their bitcoins from any device.

Individuals can create Bitcoin clients to seamlessly increase anonymity (such as allowing users to choose which Bitcoin addresses to make payments from), making it easier for non-technically savvy users to anonymize their Bitcoin transactions.

But the bigger risk for crooks and others who use bitcoin might not come from law enforcement identifying them, but from hackers who are out to rob their virtual Bitcoin wallets dry.

There have been several cases of hackers using malware to steal the currency in the virtual wallet stored on a user’s machine.

Last year, computer security researchers discovered malware called “Infostealer.Coinbit” that was designed specifically to steal bitcoins from virtual Bitcoin wallets and transfer them to a server in Poland.

One Bitcoin user complained in a Bitcoin forum that 25,000 bitcoins had been stolen from an unencrypted Bitcoin wallet on his computer. Since the exchange rate for bitcoins at the time was about $20 per bitcoin, the value of his loss at the time was about $500,000. A popular web hosting company called Linode was also infiltrated by an attacker looking to pilfer bitcoins.

And there have also been cases of hackers attempting to use “botnets” to generate bitcoins on compromised machines.

According to the FBI, quoting an anonymous “reliable source,” last May someone compromised a cluster of machines at an unidentified Midwestern university in an attempt to manufacture bitcoins. The report doesn’t provide any additional details about the incident.

Bitcoins are not mere drug currency.

Bitcoins are not failing.

Okay?

Are we clear about that?

Good.

The future of online commerce looks to rely less and less on the physical amount of money you have in your bank accounts and wallets and more on what you could call “digital” wallets: online reservoirs where you store money. Really, we already use some variation of a digital wallet, we just don’t easily acknowledge it. You work, you get paid via direct deposit, numbers change in your checking account, you use debit and credit cards to make transactions, you go back to work. Rinse, repeat. You hardly ever see cash unless you deliberately withdraw it from an ATM. Anymore, our money consists of strings of number values running through some computer located who knows where. We just confidently assume that all that money is actually staying or going where it should be staying or going.

While that describes our current model of commerce, it also serves as a fair portrait of Bitcoins, the emerging currency exclusive to the Internet.

If you’re familiar with Bitcoins and run an online business, how do you feel about accepting this form of currency? Cash currency has never kept somebody from getting ripped off, so what is the main hesitation for you and your business when it comes to accepting an exclusively online currency? If you’re unsteady about it right now, what would you like to see change with Bitcoins (or any type of online currency) before you were more comfortable with using it? Or, are you totally onboard with this form of currency already? Share your thoughts with us and other readers below in the comments.

Essentially, Bitcoins are an intangible currency, really no different in action than the numbers bouncing up and down in your bank account. Alternately, instead of representing sums of physical currency, Bitcoins are literally a majestic sequence of unique numbers that can be traded for goods. Instead of swapping wads of bound fibers and inks that are woven together into this germy thing we call cash, Bitcoins exist in a purely digital tapestry. It’s an experiment in decentralized currency, and while it’s been a good experiment and still has some growing to do, it doesn’t show any signs of disappearing anytime soon.

While it’s still got some time to really appreciate and grow stronger as a currency, a purely online currency will exist in one form or another. It won’t ever replace your tangible currency, but work alongside it for all of your online consumer decisions.

To find out more about the current state of Bitcoins and what will happen with them in the near (and far) future, I got in touch with Gavin Andresen, the Lead Core Bitcoin Developer, about the developments of the past year regarding Bitcoins and why this novel currency could feature prominently in the future of online commerce.

Bitcoins: A Primer

Money as an object is meaningless. It’s paper and and some inks and, thanks to people, lots of bacteria. It’s an arbitrary token that merely represents a commercial promissory value people can earn in exchange for goods or services that can then either be saved or spent on other goods or services. Dollars, euros, yen, pounds, rupees, tobacco leaves, rands – it doesn’t matter what object you invest value into, it’s the idea behind the currency that buttresses its value. The Bitcoin is no different.

The only difference is that, as opposed to physical money that you’ll stuff into your pockets and wallets, you will likely never actually hold a Bitcoin (yes, there are physical versions of Bitcoins if you absolutely must have a real version to thumb around in your palms). Just because you’re likely to never touch one, though, doesn’t mean that Bitcoins are any less valuable than the bills you have folded up in your right pocket. Instead, think of it like this: you are no more likely to hold a Bitcoin in your hand than you are to hold Pythagoras’ theorem in your hand.

What does distinguish this disembodied currency from its corporeal familiars, however, is that Bitcoins are not dependent on anything except the people who produce and use it. No governments, no banks, no organizations – just people. A truly anarchistic, peer-to-peer currency.

For a simplified explanation for how the Bitcoin market works on a consumer level, have a look at this video put together by We Use Coins.

The currency, however, doesn’t just fall into your lap like a prize from a cereal box, nor is it just magically conjured up from the imagination like the latest Internet meme. The production of Bitcoins is best explained through the simile of gold mining. Instead of boring through a mountain to unearth precious metals, new Bitcoins are generated by unlocking a mathematical sequence called a block chain and are doled out in increments of 50. The people that produce these Bitcoins, then, are known as miners (that’s actually the technical term for Bitcoin producers, too, not just a metaphorical descriptor). These miners, however, have traded in their helmets and pickaxes in exchange for loads of GPU firepower and very sophisticated software capable of deciphering the block chains. The software works in tandem across a network to solve these cryptographic proofs and the miner who is the first to solve the block chain will receive the 50 Bitcoins. Once a block chain has been unlocked, it is added to a ledger in order to prevent those Bitcoins from double-spending.

Eventually, as more blocks are solved, fewer Bitcoins will be generated because the block chains will be worth fewer new coins. Solving a block chain today is worth 50 new Bitcoins, but as of this December that reward will be reduced to 25 Bitcoins. Some time off in the future, it will be reduced again to 12.5. The gradual reduction in rewards works to mitigate the generation of new Bitcoins so as to avoid flooding the market, which would result in a devalued currency.

As more miners work to generate Bitcoins, the difficulty in unlocking the block chains increases so as ensure that a new block is generated only every 10 minutes on average. The increased difficulty of unlocking a block chain’s sequence is designed in such a way that, over time, the maximum capacity of Bitcoins that will be generated will be 21 million. Added to the multiplied difficulty of solving subsequent block chains, more and more computer power is required, which some have said could be a deterrent for would-be miners from working on the more difficult block chains. Andresen disagrees with the argument that hardware needs are becoming preventive. “Mining Bitcoins is becoming increasingly energy efficient,” he says. “Bitcoin miners want to pay as little as they can for electricity, so they’re constantly working to make mining more efficient.”

Energy requirements wouldn’t really matter in the grand scheme of Bitcoin production anyways, Andresen explains, as the Bitcoin production process is smart enough to adjust for variations in the miner work force. “The Bitcoin system adjusts itself so that the target number of Bitcoins are created about every 10 minutes, no matter how many miners there are.”

He adds, “The number of Bitcoin miners has almost nothing to do with how quickly Bitcoin transactions are processed, so it doesn’t matter to the Bitcoin system how much energy or how many miners are working – as long as there is one, the system will work.”

The production of Bitcoins isn’t infinite, though. In fact, there is a fixed amount that will ever be produced: 21 million. Although that peak Bitcoin mark isn’t expected to be reached until 2140, the number of Bitcoins generated will begin to taper off toward zero well before that, at which point miners will then be compensated with Bitcoin transaction fees. As the generation of Bitcoins decreases over time, the cost of a transaction using Bitcoins will increase, which these blocks exist to verify. In lieu of transaction fees, though, Andresen postulates that miners could also be compensated by a “more complicated arrangement between merchants that want their transactions confirmed quickly and securely.” One way or another, though, the monetary reward for generating Bitcoins will always be present.

As of this year, over 8 million Bitcoins have been generated. The first block of Bitcoins to be unlocked was completed by Satoshi Nakamoto, who could be considered the progenitor of Bitcoins. As Wired Magazine’s Benjamin Wallace covered extensively in a piece about bitcoins last year, Nakamoto might be best understood as the Tyler Durden of the Bitcoin culture. An effluvium of mystery envelopes Nakamoto as no one is certain of who he is or where he came from or, most intriguing, where he disappeared to following his last public communication near the end of 2010. It’s rumored the name was a pseudonym or that Nakamoto was actually a collective of developers. It’s even been suggested that Nakamoto was a nom de guerre for assorted bodies of the United States government. Nobody knows, and every major player in the Bitcoin industry denies being Nakamoto.

At this point, though, as the Bitcoin system is beginning to become more stabilized and the project is on the cusp of transcending any one person, does the origin of Bitcoins really matter anymore? It’s been around long enough to confidently assess that dealing in Bitcoins is likely not some kind of Faustian gamble. Besides, one of the prominent features of Bitcoins is its near-anonymity of the users who deal with it, a quality celebrated by Bitcoin proponents. If the currency users are mostly anonymous, why then shouldn’t the progenitor of Bitcoins be anonymous, too? If the shoe fits, right? We could all be Nakamoto and none of us would be Nakamoto. To obsess over the origin of Bitcoins threatens to belie the hard work that the currency’s current legion of developers are doing in order to bolster Bitcoins into a formidable, viable option for online commerce.

The Problem With Bitcoins

The Bitcoin has had a tumultuous twelve months. Perhaps its biggest mainstream debut to date happened in June 2011 when Gawker’s Adrian Chen published a piece about the underbelly of the Internet, the Silk Road, where you can buy, among other things, any fashion of drugs (drugs I didn’t even think existed anymore) one desires. Because of the anonymity that accompanies the use of Bitcoins, the Silk Road trades exclusively in the currency. As Gawker’s story was many people’s introduction to Bitcoins, the piece carelessly marginalized it as The Currency for underground drug trafficking on the Internet.

Regardless of Gawker’s oversights, Bitcoins blew up. The value of Bitcoins skyrocketed after Chen’s piece began to circulate and inspire interest in legions of new potential customers of Silk Road. Consequently, Senator Chuck Schumer called for a federal investigation into the Silk Roadin order to hopefully shut it down. Now that the Bitcoin market had attracted the attention of the United States government, the popularity of the currency continued skyward.

The boom was short-lived, though, as it was not an organic and sustainable growth. It was an artificial trend born from a sudden onslaught of sensational media attention that ballooned the value of the currency. Being at the mercy of the public’s caprice, though, the value of Bitcoins crashed back to Earth a month later. By August, it had returned to its pre-Gawker levels.

Five months after the Gawker piece, Wired was preparing the toe-tags for Bitcoins, citing the currency’s sustainability problems and increasing lack of interest in the continued production of Bitcoins.

Andresen concurs that Bitcoins were pushed out onto the main stage long before the system was ready to handle that kind of attention. “We had a press avalanche last year,” he says, “Where the first couple of mainstream articles about Bitcoin caught the attention of other reporters, who in turn also wrote about it, which then triggered even more press.”

He continues, “That was both great and terrible for the project: great because it drew a lot more technical and business talent to look at Bitcoin and start Bitcoin-related projects, but terrible because when people realized that Bitcoin still has a lot of growing up to do, the speculative bubble popped.”

It’s misleading to say that Bitcoins failed because of that popped bubble. True, investing in Bitcoins currently isn’t as profitable as it was for a brief period last year, but that kind of inflation was artificially generated and really should never have happened in the first place. More, it’s probably not the last time the Bitcoin will encounter some heavy turbulence. “I think it is very likely the same thing will happen again sometime in the next few years as other parts of the world discover Bitcoin or it is re-discovered in Europe and the U.S.,” Andresen says. “I expect the wild price fluctuations to diminish over time as Bitcoin infrastructure grows up and speculators start to get a better idea of the real value of Bitcoin.”

That’s Money 101 for you, though: the potent volatility of supply and demand working upon, for better or worse, the unpredictable engines of human interest. Adding to the uncertainty is the fact that, most obviously, people already have a form (if not multiple forms) of currency, which has likely created an erroneous impression for the laity that Bitcoins are a second-class currency.

Then again, Bitcoins were never really intended to launch like an unstoppable money-missile into the future. Nakamoto, Andresen, and other Bitcoin developers have always cautioned investors that Bitcoins should at best be considered an experiment. “I tell people to only invest time or money in Bitcoin that they can afford to lose,” Andresen says. “There are a lot of things that could possibly derail it, ranging from some fundamental flaw in the algorithm that everybody has missed (he doesn’t see this as a likely possibility at this point) to world-wide government regulation (also unlikely, he says) to some alternative rising up and replacing Bitcoin.”

In a way, the story thus far of Bitcoins as an unpredictable investment is the quintessential story of the Internet as a whole. Every prominent company that currently claims a seat among the pantheon of technology giants – Apple, Google, Facebook, Twitter, IBM, et al. – has come into that position due to the rise and fall of previous online ventures. The lessons gleaned from the decline of previous companies like the Myspaces and Friendsters and Lycos is likely the only reason the current generation of tech leaders have managed to prevail for so long. In the end, the diminished presence of these companies is less a woeful tale of failure and more a triumphant testament to how resilient and efficient the evolution of ideas has been on the Internet, especially in such a short amount of time.

With Bitcoins, it remains to be seen if it will eventually be minted as a mainstay in online culture or merely serve as an early milestone in the continuing evolution of online currency. Andresen is optimistic, though, that Bitcoins are here to stay even in light of competing online currencies possibly popping up in the future. “I think to overcome Bitcoin’s head-start, an alternative will either have to have a large company or government backing it and marketing it. Or else, it will have to be radically better in some way,” he says.

“There seems to be a perception that Bitcoin is in a winner-take-all race against other currencies; either everybody in the world will be using it for all of their online purchases in 50 years or it will not exist. I think the online payment world will like our current world of currencies – different currencies used in different places. The online payments won’t be divided by geography, though it might be divided by language or culture or social network.”

As it were, the currency network’s public image may have taken a bruising last year, but the reports of Bitcoin’s demise appear to have been exaggerated.

The Currency of the Future?

For now, the Bitcoin experiment appears to have weathered the Great Media Blitzkrieg of 2011. Bitcoins’ value is once again growing at the organic rate it was intended to grow at. So… to 2140 and beyond, right?

“I’m not even going to try to predict what will happen in the year 2140,” Andresen is quick to say. His focus is more attuned to the more immediate future of Bitcoins. “In December of this year, the Bitcoin will be 4 years old and the number of new Bitcoins produced will be cut in half. I think we will learn a lot when that happens and that will give some insight into what will happen over the years as Bitcoin production slowly drops to zero.”

Like any model of currency, it’d be a risk to really put all of your eggs into the Bitcoins basket. The currency could have long-term staying power. Then again, it could exist as a prototype that ends up producing a more advanced model of online currency and eventually be supplanted by something like a Bitcoin 2.0, for lack of a better term. Either way, some version of Bitcoin will continue to grow and become a part of our future experience with online commerce.

“I think there will eventually be one dominant currency that is used for 80% of worldwide online transactions,” Andresen predicts, “but I think there will always be alternatives. The most likely outcome in my lifetime, the next 40 years or so, is most people will use their national currencies when purchasing goods and services from other people in their own countries but will use something else for international payments.”

Naturally, as Bitcoins continue to evolve, developers like Andresen are working hard at ensuring the private security of Bitcoin users. Andresen says his past six months have been spent building “multi-signature transactions” for the Bitcoin network. He explains the multi-signature security feature as thus: “They are kind of like if you took all of the paper money in your wallet and then tore it in half and put half in your safe deposit box and kept the other half in your house. A robber would have to break into both your house and your safe deposit box to steal your money.”

You’d be hard pressed to find that kind of security with your current stash of cash if for nothing else but because it would be ungodly inconvenient for the consumer, to say nothing of the ambitious thief. Andresen says that’s one of the major advantages Bitcoins will have over our current terrestrial currency: you can conjunctively store your Bitcoins in two places at once so that in order to use them, a person would need access to both storage sites. One location where you might store your Bitcoins could be a secure website run by a bank which acts as the proverbial safe deposit box for Bitcoins whereas the other could be your computer or smartphone.

“To steal your Bitcoins, thieves would have to break into both your computer or smartphone andyour bank. And, it would be impossible for anybody at the bank to steal them without first breaking into your computer.”

The infrastructure for this multi-signature security technology is still in production, he says, but he expects that by the end of this year “there will be easy-to-use, incredibly secure and convenient solutions for storing and spending Bitcoins.”

With that kind of unprecedented level of security, it’s even possible that in the future Bitcoins might become a wise means for stashing your savings.

While the security advances will likely be a strong draw for future Bitcoin investors, perhaps of equal importance to the gradual growth of Bitcoins will be its acceptance as a form of payment with more online businesses, but that’s all in due time. As the reliability and legitimacy of Bitcoins is developed over time, don’t be surprised to see more online businesses begin accepting it. For now, though, the goal is to nurse the Bitcoin economy to a level where it will persevere the next blizzard of media attention the developers anticipate in the coming years. It’s possible Bitcoins may endure another “rise-and-fall” inflation in the future, but hopefully it won’t so easily shake the faith of the masses, at least as badly as last year’s roller coaster appears to have done.

In the meantime and in-between time, reconsider what those figures in your bank account really mean to you. You might see dollars or whatever your country’s currency happens to be, but the reality is that what you’re using these days intrinsically isn’t so far removed from Bitcoins. The Bitcoin experiment may or may not survive to 2140 but even if the Bitcoin itself were to disappear, the very idea of it is powerful enough that the development of an online currency will undoubtedly continue.

Bitcoin is not inherently anonymous. It may be possible to conduct transactions is such a way so as to obscure your identity, but, in many cases, users and their transactions can be identified. We have performed an analysis of anonymity in the Bitcoin system and published our results in a preprint on arXiv.

The Full Story

Anonymity is not a prominent design goal of Bitcoin. However, Bitcoin is often referred to as being anonymous. We have performed a passive analysis of anonymity in the Bitcoin system using publicly available data and tools from network analysis. The results show that the actions of many users are far from anonymous. We note that several centralized services, e.g. exchanges, mixers and wallet services, have access to even more information should they wish to piece together users’ activity. We also point out that an active analysis, using say marked Bitcoins and collaborating users, could reveal even more details. The technical details are contained in a preprint on arXiv. We welcome any feedback or corrections regarding the paper.

Case Study: The Bitcoin Theft

To illustrate our findings, we have chosen a case study involving a user who has many reasons to stay anonymous. He is the alleged thief of 25,000 Bitcoins. This is a summary of the victim’s postings to the Bitcoin forums and an analysis of the relevant transactions.

We consider the user network of the thief. Each vertex represents a user and each directed edge between a source and a target represents a flow of Bitcoins from a public-key belonging to the user corresponding to the source to a public-key belonging to the user corresponding to the target. Each directed edge is colored by its source vertex. The network is imperfect in the sense that there is, at the moment, a one-to-one mapping between users and public-keys. We restrict ourselves to the egocentric network surrounding the thief: we include every vertex that is reachable by a path of length at most two ignoring directionality and all edges induced by these vertices. We also remove all loops, multiple edges and edges that are not contained in some biconnected component to avoid clutter. In Fig. 1, the red vertex represents the thief and the green vertex represents the victim. The theft is the green edge joining the victim and the thief. There are in fact two green edges located nearby in Fig. 1 but only one directly connects the victim to the thief.

Fig. 2: An interesting sub-network induced by the thief, the victim and three other vertices.

Interestingly, the victim and the thief are joined by paths (ignoring directionality) other than the green edge representing the theft. For example, consider the sub-network shown in Fig. 2 induced by the red, green, purple, yellow and orange vertices. This sub-network is a cycle. We contract all vertices whose corresponding public-keys belong to the same user. This allows us to attach values in Bitcoins and timestamps to the directed edges. Firstly, we note that the theft of 25,000 BTC was preceded by a smaller theft of 1 BTC. This was later reported by the victim in the Bitcoin forums. Secondly, using off-network data, we have identified some of the other colored vertices: the purple vertex represents the main Slush pool account and the orange vertex represents the computer hacker group LulzSec (see, for example, their Twitter stream). We note that there has been at least one attempt to associate the thief with LulzSec. This was a fake; it was created after the theft. However, the identification of the orange vertex with LulzSec is genuine and was established before the theft. We observe that the thief sent 0.31337 BTC to LulzSec shortly after the theft but we cannot otherwise associate him with the group. The main Slush pool account sent a total of 441.83 BTC to the victim over a 70-day period. It also sent a total of 0.2 BTC to the yellow vertex over a 2-day period. One day before the theft, the yellow vertex also sent 0.120607 BTC to LulzSec. Theyellow vertex represents a user who is the owner of at least five public-keys:

Like the victim, he is a member of the Slush pool, and like the thief, he is a one-time donator toLulzSec. This donation, the day before the theft, is his last known activity using these public-keys.

A Flow and Temporal Analysis

In addition to visualizing the egocentric network of the thief with a fixed radius, we can follow significant flows of value through the network over time. If a vertex representing a user receives a large volume of Bitcoins relative to their estimated balance, and, shortly after, transfers a significant proportion of those Bitcoins to another user, we deem this interesting. We built a special purpose tool that, starting with a chosen vertex or set of vertices, traces significant flows of Bitcoins over time. In practice we have found this tool to be quite revealing when analyzing the user network.

Fig. 3: A visualization of Bitcoin flow from the theft. The size of a vertex corresponds to its degree in the entire network. The color denotes the volume of Bitcoins — warmer colors have larger volumes flowing through them. We also provide an SVG which contains hyperlinks to the relevant Block Explorer pages.

Fig. 4: An annotated version of Fig. 3.

In the left inset, we can see that the Bitcoins are shuffled between a small number of accounts and then transferred back to the initial account. After this shuffling step, we have identified four significant outflows of Bitcoins that began at 19:49, 20:01, 20:13 and 20:55. Of particular interest are the outflows that began at 20:55 (labeled as 1 in both insets) and 20:13 (labeled as 2 in both insets). These outflows pass through several subsequent accounts over a period of several hours. Flow 1 splits at the vertex labeled A in the right inset at 04:05 the day after the theft. Some of its Bitcoins rejoin Flow 2 at the vertex labeled B. This new combined flow is labeled as 3 in the right inset. The remaining Bitcoins from Flow 1 pass through several additional vertices in the next two days. This flow is labeled as 4 in the right inset.

A surprising event occurs on 16/06/2011 at approximately 13:37. A small number of Bitcoins are transferred from Flow 3 to a heretofore unseen public-key 1FKFiCYJSFqxT3zkZntHjfU47SvAzauZXN. Approximately seven minutes later, a small number of Bitcoins are transferred from Flow 3 to another heretofore unseen public-key 1FhYawPhWDvkZCJVBrDfQoo2qC3EuKtb94. Finally, there are two simultaneous transfers from Flow 4 to two more heretofore unseen public-keys:1MJZZmmSrQZ9NzeQt3hYP76oFC5dWAf2nD and 12dJo17jcR78Uk1Ak5wfgyXtciU62MzcEc. We have determined that these four public-keys — which receive Bitcoins from two separate flows that split from each other two days previously — are all contracted to the same user in our ancillary network. This user is represented as C.

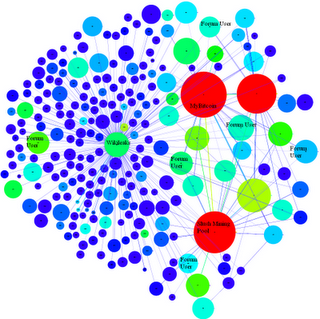

There are several other examples of interesting flow. The flow labeled as Y involves the movement of Bitcoins through thirty unique public-keys in a very short period of time. At each step, a small number of Bitcoins (typically 30 BTC which had a market value of approximately US$500 at the time of the transactions) are siphoned off. The public-keys that receive the small number of Bitcoins are typically represented by small blue vertices due to their low volume and degree. On 20/06/2011 at 12:35, each of these public-keys makes a transfer to a public-key operated by the MyBitcoin service. Curiously, this public-key was previously involved in another separate Bitcoin theft.WikiLeaksWikiLeaks recently advised its Twitter followers that it now accepts anonymous donations via Bitcoin. They also state that “Bitcoin is a secure and anonymous digital currency. Bitcoins cannot be easily tracked back to you, and are a [sic] safer and faster alternative to other donation methods.” They proceed to describe a more secure method of donating Bitcoins that involves the generation of a one-time public-key but the implications for those who donate using the tweeted public-key are unclear. Is it possible to associate a donation with other Bitcoin transactions performed by the same user or perhaps identify them using external information?

Fig. 5: A visualization of the egocentric user network of WikiLeaks. We can identify many of the users in this visualization.

Our tools resolve several of the users with identifying information gathered from the Bitcoin Forums, the Bitcoin Faucet, Twitter streams, etc. These users can be linked either directly or indirectly to their donations. The presence of a Bitcoin mining pool (a large red vertex) and a number of public-keys between it and WikiLeaks’ public-key is interesting. Our point is that, by default, a donation to WikiLeaks’ ‘public’ public-key may not be anonymous.

Conclusion

This is a straight-forward passive analysis of public data that allows us to de-anonymize considerable portions of the Bitcoin network. We can use tools from network analysis to visualize egocentric networks and to follow the flow of Bitcoins. This can help us identify several centralized services that may have even more details about interesting users. We can also apply techniques such as community finding, block modeling, network flow algorithms, etc. to better understand the network.

Feedback

We are excited about the Bitcoin project and consider it a remarkable milestone in the evolution of electronic currencies. Our motivation for this work has not been to de-anonymize any individual users; rather it is to illustrate the limits of anonymity in the Bitcoin system. It is important that users do not have a false expectation of anonymity. We welcome any feedback or comments regarding the preprint on arXiv or the details in this post.

<

<

Bitcoin’s market price since last month Photograph: blockchain.infoThe maximum possible number of Bitcoins that can exist is 21m, meaning that at present prices the currency would be worth just over $3bn. Trades can be made with fractions of Bitcoins, providing flexibility that enables transactions.

Bitcoin’s market price since last month Photograph: blockchain.infoThe maximum possible number of Bitcoins that can exist is 21m, meaning that at present prices the currency would be worth just over $3bn. Trades can be made with fractions of Bitcoins, providing flexibility that enables transactions.

{kind=link}